What factors caused the sharp rise in tungsten prices

Overview

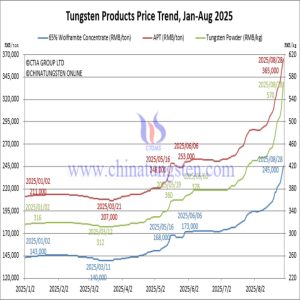

As a strategic metal known as the “industrial tooth,” tungsten prices have surged rapidly over the past two months. From 378 yuan per kilogram in early July, it surged to 580 yuan per kilogram by late August—a 53% increase. This explosive growth has not only shaken the market but also triggered a chain reaction across the entire industry chain. The reasons behind this price surge lie in the combined effects of supply-demand dynamics, policy adjustments, and international developments.

Core Factors

Supply-Side Tightening

– China’s Export Control: Implementing “one order, one certificate” management for 25 tungsten products including ammonium paratungstate

– Total Mining Quota Control: 2025’s initial mining quota reduced to 58,000 tons, down 6.45% year-on-year

– Environmental Production Cuts: Central environmental inspections triggered production restrictions and rectifications at multiple mines, reducing operating rates below 35%

– Resource Depletion and Rising Costs: China’s average tungsten ore grade declined from 0.42% in 2004 to 0.28% in 2024

Demand Expansion

– Defense Sector: Global military spending surpasses $2.3 trillion; China’s defense tungsten product orders surge 42% YoY

– New Energy Sector: Photovoltaic tungsten filament penetration rate jumps to 60%; Lithium tungstate cathode material demand for solid-state batteries surges 300% YoY

– Industrial Sector: Traditional demand for cemented carbides and specialty steels maintains steady growth

Market Sentiment and Dynamics

– Strong reluctance among holders to sell, scarce low-priced inventory

– Inverted domestic-international price spread, with China’s APT prices exceeding European markets

Conclusion

This surge in tungsten prices represents a revaluation of strategic mineral resources amid global geopolitical dynamics, industrial upgrading, and resource competition. It underscores the growing importance of strategic minerals and signals impending restructuring within related industrial chains.